Spring emerges with hope

Spring emerges

with hope

Stronger US economic and profits data have supported equity markets over the past month. Indeed, with better than expected economic data, both in terms of robust growth and continued falling inflation (including wage inflation) the Federal Reserve may consider that they have guided the US to a soft-landing.

Despite falling inflation, the better-than-expected economic growth has seen the Federal Reserve guiding investors away from expecting rapid interest rate cuts through 2024. On the back of a revision to expectations, bond yields have moved higher since the beginning of the year.

Markets are still discounting more rate cuts than the Federal Reserve is suggesting, so unless economic growth slows further or inflation comes in lower (better) than expected, lower bond yields may be delayed.

Recent updates suggest that in Europe and the UK, economic performance and profits have been disappointing which has resulted in these regions lagging the US equity market.

The better US economic backdrop took on another tone as lending conditions improved, as signaled by the Senior Loan Officer Survey. This historically has predated improvements in corporate borrowing, investment and employment.

Despite the good news from survey data, there is a latent risk in the form of bad debts arising from the fall in values within Commercial Real Estate (CRE), especially offices. Banks that have lent into the US CRE market are finding the need to provide for bad loans. Bad debt provisions are expected to amount to many hundreds of millions of US Dollars. Most of these loans are contained within the US banking system, but bad debt write offs are popping up in Japanese and European banks too. Whilst regulators appear sanguine about the systemic risks, it is a subject that we will keep a wary eye on as the outlook for 2024 appears to be otherwise brightening.

Despite the UK economy stagnating there are signs of hope. The housing market is potentially showing daffodil like emergence after a long period of stagnation. The increase in new buyers and mortgage applications should be reflected in a recovery in house prices. Hopefully this will also result in a recovery in the wider economy and new house building which has fallen back to decade lows.

Mission accomplished: Soft landing?

Investment commentators (including ourselves) have been wary about the state of the US economy. Fears and forecasts of a recession, due to the impact of higher interest rates, have been present since the end of 2022.

However, despite the US housing market stagnating and a weak manufacturing backdrop, the US consumer has kept on spending and a recession has been avoided. The resilience of the US economy contrasts with the wider woes in Europe and the UK, where economic growth has been stagnant and China where a worsening real estate crisis appears to be creating a backdrop for deflation. It may also potentially become a replay akin to Japan's lost decade in the 1990s

We would suggest that fiscal policy in the US, which saw an unexpected rise in the Government Deficit in 2023 (i.e. the government chose to stimulate higher economic growth through policy choices) resulted in a better economic backdrop than those countries pursuing austerity.

Due to continued economic growth, low unemployment has resulted. An unemployment rate less than 4% typically implies that the US labour market remains tight. Somewhat surprisingly wage inflation has eased without an increase in unemployment, surely a win for policymakers.

Mission accomplished: low unemployment and falling wage inflation

Source: Bloomberg, Artorius

Although wage inflation is falling, which eases the need for higher interest rates, the rate of wage inflation is still high relative to historical norms. We suggest that for interest rates to be reduced by as much as the market is discounting either unemployment will need to rise or wage inflation will have to continue to fall.

US Federal Reserve policymakers of late have indicated that they are wary of cutting interest rates too soon and by too much. This delay has resulted in a small rise in bond yields since the start of 2024.

But whilst cuts to interest rates may be delayed, the combination of resilient economic growth and lower inflation suggests that a ‘soft-landing’ has been achieved. No recession and the resultant combination of low unemployment and high inflation has been tamed, at least for now.

For that, the policymakers in the US, both fiscal and monetary, should be congratulated for achieving a soft-landing.

Earnings: US exceptionalism

Companies on both sides of the Atlantic are drawing towards the end of their quarterly updates. Through the last few months of 2023, expectations were reduced. Unsurprisingly, the lowered bar has generally been beaten in the most recent updates.

There is a contrast between the US and the rest of the world. Expectations for US earnings-per-share (EPS) continue to drift upwards whilst the rest of the world has seen a slight reduction in recent weeks.

The striking thing about the weakness in non-US EPS is that the US Dollar has been strong, which normally provides a boost for non-US earnings.

This supports the notion that despite elevated valuations, the US equity market may continue to be supported by stronger fundamentals.

Earnings expectations continue to recover in the US but have fallen back elsewhere

Source: Bloomberg, Artorius

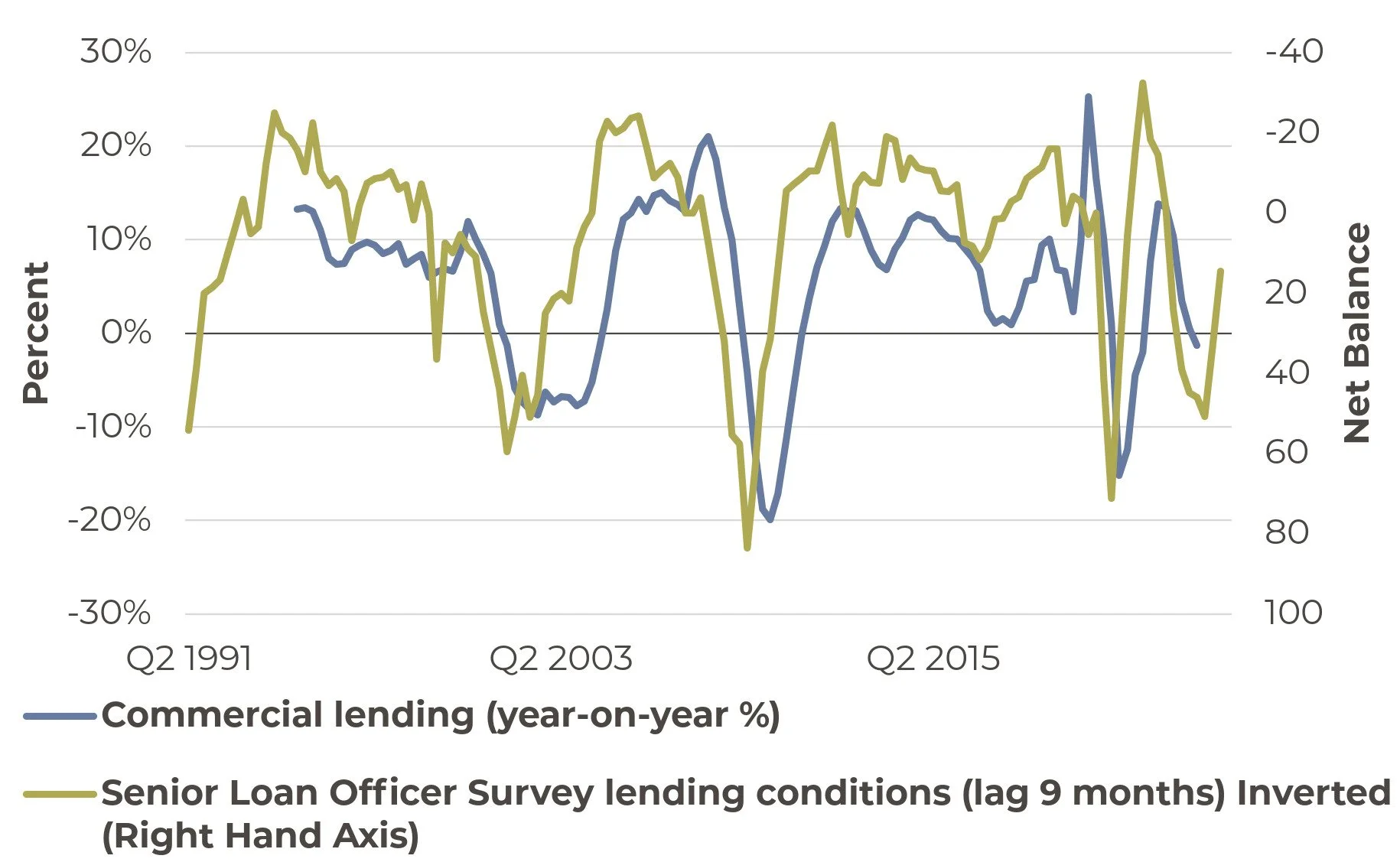

Senior Loan Officer Survey

An important but overlooked indicator for the US economy is the Federal Reserve Senior Loan Officer Survey (SLO). The survey reflects bank lending conditions in the US economy. It measures the degree to which banks are changing covenants and borrowing terms. The recent SLO survey points to an easing in lending conditions.

Easier lending conditions should be supportive for the US economy. When the SLO falls (signalling banks moving to less restrictive lending conditions) the rates of growth in employment, investment, and profits tend to improve.

The Senior Loan Officer Survey suggests that banks are easing lending conditions, typically this results in a recovery in commercial lending and correspondingly employment and profits

Source: Bloomberg, Artorius

Built on sand?

On the back of better than expected economic growth and profits, it is tempting to become quite sanguine about the state of the world.

However, a cautionary tale is emerging from the US commercial real estate (CRE) sector. The post-Covid recovery has seen a change in work patterns. Working-from-home (WFH) has seen office occupancy fall from over 60% to 40-45% according to Deloitte Consulting.

As office vacancies increase so the value of the offices fall, and as much of the real estate is encumbered with debt (a bit like housing and mortgages), bad debts are now emerging as office owners renege on their debts. With $560 billion of loans maturing by the end of 2025, banks are facing up to the reality that the offices that they have lent against may be worth less than the loan provided to purchase them.

A number of banks have reported significant increases in bad debt provisions in recent weeks. Smaller US banks have up to 35% of their loan book exposure to the CRE sector (up from less than 15% in 2009).

These difficulties are reflected in the New York Community Bank report of higher bad debts, resulting in their own bonds being downgraded to junk status and a 38% fall in its share price on 7th February.

However, given the scale of US CRE lending, the bad debts are also showing up in non-US banks. Second tier regional German bank Deutsche Pfandbriefbank, a Bavarian lender specializing in commercial real estate finance with a large exposure to the US, saw its bonds collapse as potential losses could impinge on the bank’s credit rating. Japan’s Aozora Bank reported its first loss in 15 years also due to bad loans in US CRE.

In the view of the US Federal Reserve, these risks lie outside of the largest banks in the US. As such, the risk is not seen a systemic. Whether this proves to be too sanguine a view time will tell. Notably, the incidence of bad debts is being felt around the world and may prompt a change in lending behaviour.

Just like shopping malls went through a long process of devaluation as the impact of the internet changed shopping habits, we would suggest that the implications of the WFH revolution will take a long time to work through the financial system.

UK housing: spring forth

Whisper it quietly, but the UK economy may be on the mend. It may be optimistic daffodils or longer days meddling with the mind, but there are signs in the UK housing market that 2024 may be a year of recovery.

The Royal Institution of Chartered Surveyors (RICS) have a monthly survey which takes the temperature of the housing market. The January 2024 RICS UK Residential Survey results continue to depict a turnup in housing market activity. This is in sharp contrast with the collapse in activity through much of 2023.

The New Buyers Enquiries indicators points to a recovery, with households searching for homes to buy. Whilst interest rates are much higher than they were post-Covid, with longer mortgage terms (i.e. shifting from 25 years to 35) and a stabilisation of the interest rate cycle, buyers are buying again.

A recovery in the housing market may be on the cards for 2024

Source: Bloomberg, Artorius

The recovery in the RICS survey is also showing up in the rise in mortgage applications. Whilst the series is volatile, together with the RICS data, it implies house prices may rise through 2024.

Mortgage applications are starting to rise again normally signalling a recovery in house prices for 2024

Source: Bloomberg, Artorius

After the turbulence resulting from the unfunded tax cuts and chaos of the Autumn Budget of 2022, the market may be hoping for fiscal responsibility in the March 7th Budget, despite the short-term pressures of a potential General Election in 2024.

This recovery in house prices will hopefully result in firmer economic growth in the UK economy. This in turn will generate tax revenues and ease the fiscal constraints in coming years, reducing the need for further cuts to public spending.

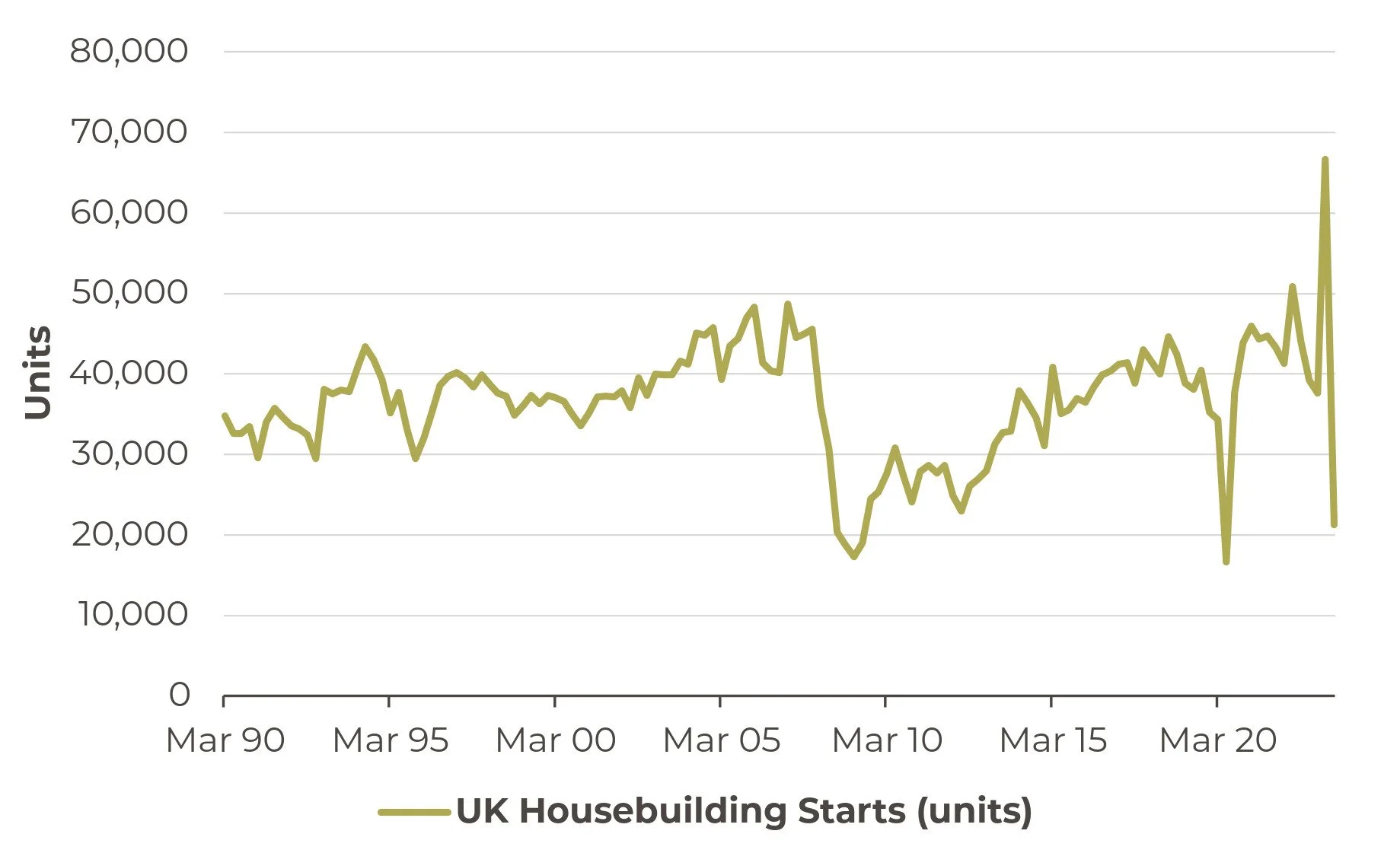

In addition, the recovery in house prices may also see a revival in housebuilding. New housing starts in 2023 fell sharply from 2022 levels. With the UK population expected to grow by 10% over 15 years and top 73 million in coming years, homes are in short supply and thus prices are likely to continue to rise.

UK housebuilding has collapsed in 2023 despite continued population growth

Source: Bloomberg, Artorius

The most striking (and niche) chart that passed my desk in recent days was the number of bricks being delivered in the UK.

Brick deliveries have headed back towards Covid lockdown lows.

Source: Bloomberg, Artorius

The potential upturn in the housing market suggests that the £2.5billion merger between two of the UK bigger housebuilders (Redrow and Barratt Homes) announced on February 7th could be timely and well-placed to reap the industry’s rewards as further consolidation strengthens a potential oligopoly in the UK house builder sector.

Naturally, the optimistic take on a potential housing market recovery comes with a caveat, not for nothing is economics known as the dismal science. If the UK housing market does recover, the Bank of England may limit the extent to which it will cut interest rates. Every silver lining has a cloud.

*Any feedback provided can be anonymous

Mission accomplished

Stronger US economic and profits data have supported equity markets over the past month. Indeed, with better than expected economic data, both in terms of robust growth and continued falling inflation (including wage inflation) the Federal Reserve may consider that they have guided the US to a soft-landing.

Recent updates suggest that in Europe and the UK, economic and profits have been disappointing which has resulted in these regions lagging the US equity market.

Against a broad set of data that is robust in the US, it is worth noting the rise of bad debts emerging from the Commercial Real Estate (mainly office) sector. Post-Covid work patterns and lower office occupancy is seeing office valuations decline and bad debts on associated lending rise.

Despite the UK economy stagnating there are signs of hope. The housing market is potentially showing daffodil like emergence after a long period of stagnation. The increase in new buyers and mortgage applications should be reflected in a recovery in house price inflation.

Important Information

Artorius provides this document in good faith and for information purposes only. All expressions of opinion reflect the judgment of Artorius at 16th February 2024 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content.

The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results.

Nothing in this document is intended to be, or should be construed as, regulated advice. Reliance should not be placed on the information contained within this document when taking individual investment or strategic decisions.

Any advisory services we provide will be subject to a formal Engagement Letter signed by both parties. Any Investment Management services we provide will be subject to a formal Investment Management Agreement, which will include an agreed mandate.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20240216001