Thanksgiving?

Thanksgiving?

As we approach the end of November, investors can say thank you for a period of strong investment returns as equities have rallied after a soft third quarter. However, these returns have been distinctively “America first” as US equities have significantly outperformed the rest of the world driven by a combination of strong earnings, a robust economy, and the hope that Trump will deliver tax-cuts. Other regions are suffering from weaker economic growth, weaker earnings, and the threat of tariffs when the President elect takes office next year. US equities thus far seem immune to the self-inflicted damage that tariffs and mass deportations would have on the economy were they to be enacted, but certain sectors (most notably healthcare) have been impacted by the potential policies of the new administration, for which we have now seen most of the potential cabinet nominees. The bond market is more alive to the inflationary impact of these policies and the risks of higher fiscal deficits and higher government debt, which has seen bond yields rise as the expectations for interest rate cuts are dialled back.

US equity outperformance has reaccelerated over the last 2 months

Source: Artorius, Bloomberg

US = S&P 500 index performance, World ex US = MSCI World ex US index performance

We recently wrote about the travails of Germany, where economic growth has been disappointing, but a wider malaise seems to be settling over the continent with economic indicators weakening. European earnings have also been relatively weak compared to their US peers and this has led to disappointing equity performance. Allied to this weakness, the European Central Bank is cutting interest rates faster than other major regions and this is leading to a weakening Euro. While longer-term lower interest rates and a weaker currency should be supportive of the economy, in the short term this is impacting performance.

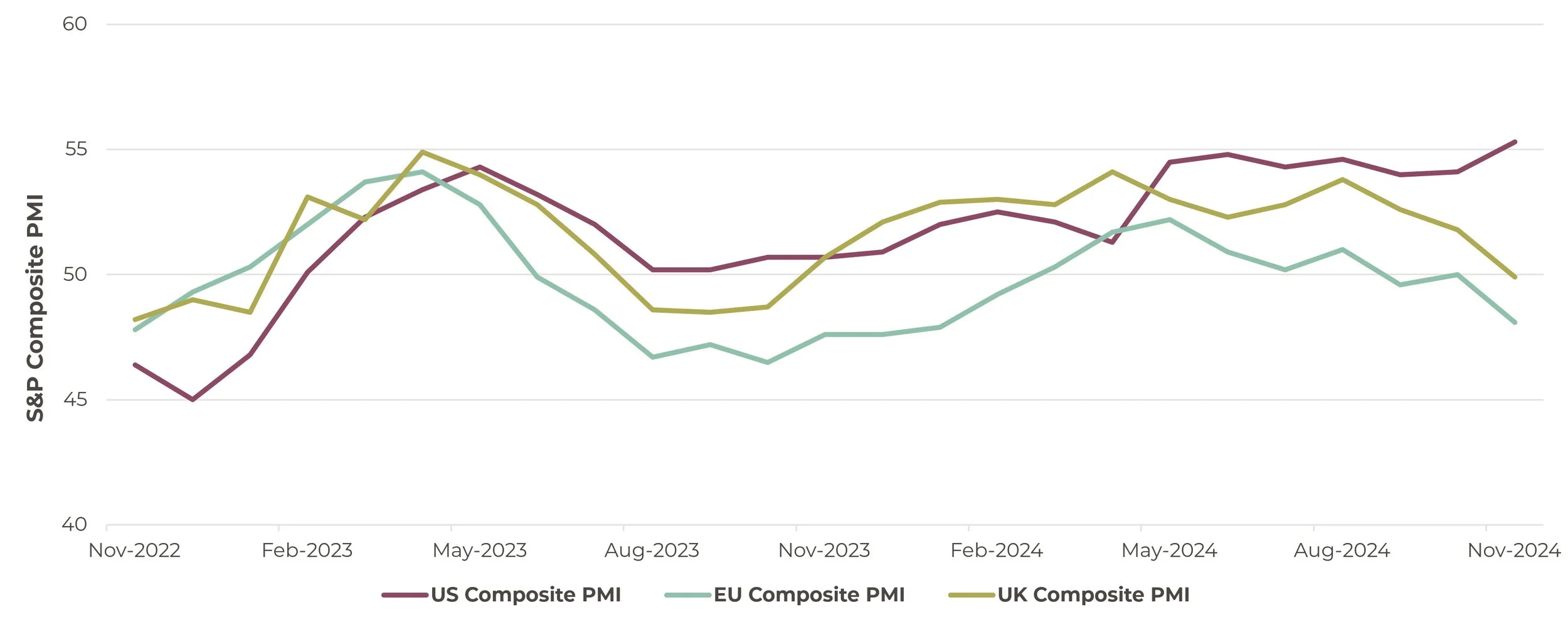

The UK had looked in a somewhat better situation but recent data suggests that the economy may be faltering. The latest PMI survey which is an indicator of economic strength, fell below 50 for the first time in over a year, which is an indication of economic contraction. Recent inflation data was higher than expected reducing the likelihood of another interest rate cut in December. Additionally business confidence has fallen after the budget and recent retail sales data was weak. If there was any doubt, the honeymoon period is over for the new government.

The US economy continues to outperform the rest. Europe is sagging.

Source: Artorius, Bloomberg

PMI – Purchasing Manager Index. This is an indicator of the prevailing direction of economic trends in the manufacturing and service sectors. The indicator is compiled and released monthly by S&P Global. Above 50 suggests that the economy is growing and below 50 contracting.

No Black Friday sales

The upshot of this continued American exceptionalism is that valuations are high, particularly in comparison to the rest of the world. Market leading companies delivering better earnings (see our recent Investment Outlook), supported by a robust economy and potential tax-cuts certainly deserve a premium rating, but that premium is at a 10 year high and growing – for discounts you need to look elsewhere.

US Valuations are high and the rest of the world is trading at a significant discount

Source: Artorius, Bloomberg

We have recently switched some money out of the US mega-caps, where much of the valuation premium exists, into US mid-caps, a much cheaper segment of the market. But one should be aware that valuation risks exist and this caps our expectations for longer-term equity returns with the next 10 years unlikely to match the previous 10.

Gareth Thomas

Head of Investment Management

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 29th November 2024 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20241129001