Five Years On: A Remote Recovery

Five Years On: A Remote Recovery

This week marks the sombre anniversary of the World Health Organisation declaring Covid-19 a global pandemic. Whilst many are understandably keen to move on and forget the events that unfolded, this week we look back at the five years in markets since Covid and how the world has changed.

Market Performance

The S&P 500 reached its lowest point during the pandemic on 23rd March 2020, closing at 2,237.4, down by over a third from a record high less than a month prior. Companywide emails were sent telling employees to temporarily work from home with the optimistic outlook that things would get ‘back to normal’ soon. Things did not get back to normal. The economic fallout was swift and severe, with tens of millions of jobs lost as a wave of business closures swept the globe. An unprecedented simultaneous collapse of supply and demand triggered the most severe global recession in a century. This saw the FTSE 100 and S&P 500 indices plummeting the furthest since Black Monday in 1987.

No one knew how long the pandemic would last. Markets, however, were quick to recover and reached record highs by August 2020. The chart below shows a comparison of major markets, reported in their native currency in the five years since the low of March 2020 (MSCI All Country World Index (ACWI) and Emerging Markets (EM) are reported in US Dollars).

Performance of markets since Covid bottom

Source: Artorius, Bloomberg

In markets there has been a clear winner: the US. The American market headlined by the ‘Magnificent Seven’ has dominated, as shown by the performance of the S&P 500 above. This has also dragged the MSCI ACWI higher as the index is heavily weighted to the US (approximately 66%). Other markets such as the UK and Emerging Markets have significantly lagged.

“You’re muted”

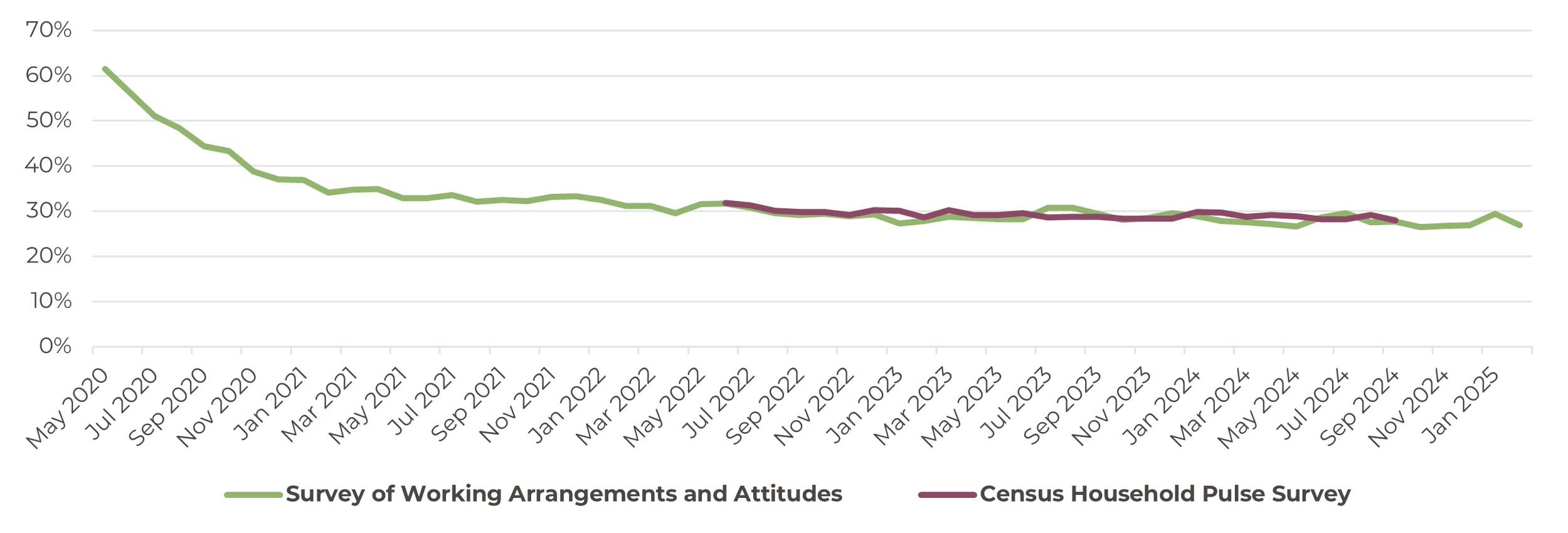

Perhaps the most significant and lasting change brought about by the pandemic is the widespread adoption of working from home. The familiar setting of meetings held in boardrooms were quickly replaced by video calls in a matter of weeks. The latest research in the US shows that roughly one quarter of all workdays are now work-from-home, signifying a drastic change from pre-pandemic working patterns.

Using a mix of household surveys, entry swipes and location data shows that work from home has become a new permanent feature of the labour market, with all indicators moving sideways since 2023, as seen in the chart below.

% of full days worked from home

US security company Kastle Systems’ ‘back-to-work’ barometer has shown that office occupancy rates have stabilised at around 55% of 2019 levels. This barometer is a weekly report that tracks office occupancy rates across 10 major US cities by analysing aggregated and anonymised building access data.

Analysis of the data reveals that hybrid work has become the norm for many, with employees valuing the flexibility it offers. Nevertheless, the gradual upward trend of office occupancy suggests businesses and employees are finding greater value in in-person collaboration. A longer-term adjustment is certainly taking place where companies refine their hybrid strategies to balance flexibility with the benefits of face-to-face engagement. This however is giving businesses the challenge of aligning workspace utilisation with evolving attendance patterns, ensuring they strike the right balance between operational efficiency and employee flexibility.

Conclusion

“There are decades where nothing happens; and there are weeks where decades happen” - Vladimir Ilyich Lenin.

Even though Covid was five years ago, the effects are still being felt across markets today. The efforts by governments to tackle the pandemic triggered record debts, hit labour markets and shifted consumer behaviour. Fuelled by post-lockdown spending, government stimulus packages and shortages of labour and raw materials, inflation peaked in many countries in 2022. The higher interest rates experienced since are a result of rampant inflation over the past three years which, amongst other factors, has a direct link to the global supply chain backlog caused by the virus.

Trump’s second term has so far threatened to blow up the world order and status quo. European countries are coming under increasing pressure to re-arm to cope with Russian aggression and Donald Trump’s efforts to reduce American expenditure on European defence. The UK is currently spending approximately £105bn on debt interest payments, nearly twice as much as they commit to defence spending. This reflects a broader trend across the West. The OECD have reported debt interest for the world’s wealthiest countries totals $2.1 trillion, dwarfing the $1.2 trillion spent on military equipment. Stubbornly high debt levels after the pandemic and the energy crisis will mean many countries like Britain will have fiscal challenges to deal with in the face of sluggish growth forecasts and cost pressures from increased military spending.

Just this week, UK chancellor Rachel Reeves demonstrated these fiscal challenges, announcing big welfare cuts and spending reductions while adding to defence spending. Many political commentators are predicting further cuts this autumn, in addition to the £40bn worth of tax rises announced during Labour’s autumn budget last year, while the demand for increased defence spending may well escalate further. Reeves is also shackled by her own fiscal rules (set just a few months ago) and a desire to avoid a Truss-like meltdown in bond markets. However, Germany is showing us that there is another way - by unlocking the constitutional debt brake the government is able to unleash significant investment into defence and infrastructure projects. Of course, the starting point matters. Germany’s finances are in a much better state than the UK (or the US) with a debt to Gross Domestic Product (GDP) ratio of just 63% compared to roughly 100% in the UK. This gives them scope to add stimulus without creating a crisis, which should support European equities more widely and is one of the drivers for our increased allocation to the region.

Whilst many prefer to avoid dwelling on the pandemic (understandably so), analysing its market impact and any lasting effects offers valuable insights to investors. And a lot has happened since. The US Capitol was attacked to try to overturn an election, Russia invaded Ukraine, Donald Trump launched a trade war – and until a month ago, the markets were at record levels, despite the bear market of 2022.

Looking back at recent events reinforces the inherent difficulty in successfully trading around news cycles. A disciplined approach to investing with a diversified asset allocation remains the recommended strategy for delivering long term returns.

Yuval Peshchanitsky

Portfolio Analyst

*Any feedback provided can be anonymous

Important Information

All expressions of opinion reflect the judgment of Artorius at 28th March 2025 and are subject to change, without notice. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete; we do not accept any liability for any errors or omissions, nor for any actions taken based on its content. The value of an investment and the income from it could go down as well as up. The return at the end of the investment period is not guaranteed and you may get back less than you originally invested. Past performance is not a reliable indicator of future results. Nothing in this document is intended to be, or should be construed as, regulated advice. Artorius provides this document in good faith and for information purposes only. Reliance should not be placed on the information contained within this document when taking individual investments or strategic decisions.

Artorius Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Artorius is a trading name of Artorius Wealth Management Limited.

FP20250328001